But then I remembered that I was trying to retire in about six years. Might my annual spending figure be important to figure out before then?

No one ever claimed that I knew what I was doing with money.

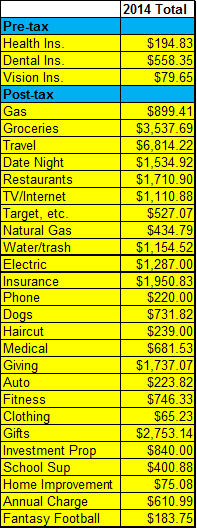

So, after many cuts and pastes, I finally had our 2014 spending figure: about $31,000. This will seem impossibly low to some people (note: we no longer pay a mortgage) and a little high to others. Travel was by far the biggest line item, weighing in at just under $7k. This is definitely higher than we normally would aim for, but we had a wedding trip to the big island of Hawaii, two trips to South America, and some domestic travel...a lot of it happening without travel hacking. Our second largest expense was groceries, followed by gifts, of all things. There's a sweeping criticism of our values in there somewhere.

For the voyeurs lurking on this blog, and those readers who miss Budget Porn, here's a taste, you pervs.

As rules of thumb go, I suppose the 4% Rule a good one to start with. It gives us a specific target for our retirement nest egg to be achieved by a certain date, which we know is more motivating and effective than "just saving as much as we can".

But even if the 4% Rule is perfectly sound, there's already a problem with my approach: that $31,000 is not a true average of our household spending. It's just what we spent last year. And even if I spend the same amount next year, and the following one, it's still not going to be representative. Let me explain.

Planning for early retirement based on my annual spending does not account for those future costs that are rare, but are surely coming. Every so often (and fairly predictably, too), I will need a new roof. Every ten to fifteen years, I will purchase another used car. Some time in my life, I will suffer a major injury or sickness that forces us to actually spend to our deductible. Kids will need braces. And so on.

My amateur budgeting misses these costs entirely, since they are not in my budget most years. And because we are in an all-out sprint to "financial independence" it's possible that we won't see any of these rare events by the time I'm forty. But some day, those costs will come around, and I will never have accounted for them in my DIY 4% calculations.

While last year may account for all my spending down to the penny, and I might even repeat that process for the next five years...that's not a reliable average. My early retirement plan creates a too-small data set, and one that skews the data in the wrong direction.

This points to the need for some real financial planning advice...you know, from a financial planner.

For those of us committed to a DIY financial planning approach, we should at least utilize a replacement cost method: budgeting in 1/20th of a cost of a 20 year roof into my annual spending, along with 1/10th of a used car, 1/10th of our insurance deductible if we assume a major medical event every decade, and so on. While that only addresses those rare costs that we know are coming, it's better than nothing.

Accounting for just those three items (a roof every twenty years, a car every ten, and one major medical event a decade), our annual spending is really $1,500 higher than the $31,000 I calculated: a 4.8% increase.

Using the 4% Rule again, the amount we'd need for retirement is not just $775,000, but $812,500: a $37,500 delta. Saving that extra $37k will be no small feat, but it would be especially hard had I only realized I'd underfunded my retirement after I gave up my employment.

In general, my DIY, amateur financial blogger approach leads me to underestimate my true spending average. Worse, it leads me to severely underestimate the amount we will need to adequately fund our retirement. For someone planning to leave the workforce very early, in the hopes of living off a nest egg for fifty years, this is particularly stupid and dangerous.

Maybe we should budget in a few dollars for a financial planner this year.

*Photo is from kvanhorn at Flickr Creative Commons.

Fantasy football? Are you Ruxin in disguise?

ReplyDeleteThe mistake I see a lot of my clients make is to anchor spending in retirement to spending now. Some parallels will apply. If you don't move, then you know that property taxes will be, adjusted for inflation or annual rises, what they are now. However, your lifestyle in retirement will be different. You may travel more. You may commute less. If you have employer-sponsored healthcare, then you need to account for paying for health insurance (and funding the HSA). You might cook in because you have more time to cook, or you may go the opposite way because you socialize more.

So, the goal is to create the retirement budget based on the lifestyle that you'll have *in retirement*, not the lifestyle you have now. And then pad it by some, because being retired and then realizing that you didn't have enough money saved and having to go back to work is almost as difficult as living in privation because you didn't have enough money socked away.

When I started playing fantasy, I was closest to Taco. These days, I feel like Andre.

DeleteI hear you on the anchoring. It's something I'm definitely doing. The health insurance is probably the one I'm not fully accounting for yet: and it's a biggie.

For now I'm aiming for $1M in investments just to pad it, as you noted. We'll have a little extra padding from the rentals, should we keep them. But this is not a great replacement for actually doing the work of estimating our retirement spending.

Maybe I can start to tackle that in a future post. Thanks for the help, Jason.

Haha I'm loving The League references! Epic show.

DeleteIt's interesting you mention health insurance. I work at a health insurance company (albeit currently on the health services side) and was reading about Medicare today. Now, I know plenty about Medicare but not at a really detailed level. What's scary to read about is just how little people have saved (not just for health care, but for retirement as a whole) and just how expensive Medicare can be for retirees. My grandma and grandpa are into their 80s now and (unfortunately) are both experiencing some pretty big medical issues. My grandpa was always one of the healthiest guys I know and it's tough to accept but high health care expenses truly are unavoidable when you age.

With that being said you can only be so conservative when it comes to retirement savings. Eventually you have to set a number and say "good enough." As someone in their mid-20s who wholly expects to work at least 3 more decades, I don't get too into the details with my retirement planning yet and I'm really just focused on getting started.

Good point about the healthcare costs very late in life. When we get a financial planner, the far out projections are part of what I hope can be gained when paying for those services. I'd just be guessing at those now.

DeleteSorry to hear about your granparents' medical situation. It's sad seeing our loved ones get old sometimes.

I think you're going to be in a good, and less risky, situation since you'll be working into your fifties. That provides a chance for a huge nestegg, and one that can cover a lot of 'what ifs'.

DBF, at it again! Why do you always have to go and ruin the fun? Here I was, wonderfully and blissfully ignorant of my potential financial planning blunder, and you come along and toss cold water on me. Jerk. Why don't you just go peddle your financially sound advice elsewhere, huh? :-)

ReplyDeleteIf I can throw water on someone's dreams, then I've done my job today.

DeleteI think this is something a lot of Mustachians may not be accounting for. And most of us don't have a blog raking in crazy money, either.

Good points here. I try to save up for things I know are coming down the road, but right now my budget is very tight since i'm trying to pay off my credit card debt. I do still put aside a bit for house and car maintenance, but not as much as I really need to be saving. Thanks for the reminder.

ReplyDeletePaying off credit card debt is probably the best guaranteed return you'll ever see in your lifetime, so kudos for focusing on that first, Kayla.

DeleteFor us, paying down debt laid the foundation of good financial habits that allows us to invest now.

I don't think 31K is bad at all for 2 people - especially with all that travel. I also think that while you might have unexpected expenses later in life, you also might not be spending that much on travel every year, so it will all even out. And some of this depends on your definition of "retired." If you develop some passive income streams, then you can look at your nest egg as more of a supplement than what you're living on.

ReplyDeleteAnyhow, when I calculated my spending it came out to around $17.5 for the year:

http://ecocatlady.blogspot.com/2015/01/what-i-spent-in-2014.html

And, as you might expect, the biggest expense was the cats! Oy!

That's incredible: $17.5k is an admirable number, and one that allows for a lot more wiggle room in financial planning.

DeleteI must have missed that post...will go back and dig in. Thanks!

Having that yearly spending figure does come in handy, but I hear you on it being slightly tedious to add up (especially when working just with spreadsheets). I think it's important to realize our needs are always changing - what we're spending on now we might not spend on in retirement, and vice versa. We have to keep that in mind and adjust for it. Either way, I'm big on padding for "just in case" scenarios, and I'm trying to focus on living lean now so retirement will cost less!

ReplyDeleteJason Hull made that same point about expenses being different in retirement. Yet another reason that planning for retirement based off our current spending has some pitfalls.

DeleteI'm also pretty conservative, and we plan for just in case/worst-case scenarios a lot. We'd much rather be safe than sorry.

Great to see you pull together your 2014 spending DB40 - now I know you're serious about hitting financial independence in 6 years!

ReplyDeleteIt's a great point about those 'one-off' expenses that can happen every few years, or big items that might be 5 or 10 years down the track. Taking an annualised proportion of those is important for estimating your 'true' effective annual spending, but identifying them can be the hard part!

Coincidentally, I just put up a detailed financial model on my blog that allows you to input all of these future 'one-off' items and other potential future changes to income and expenses, and see the impact on your retirement date. It doesn't quite tell you what might happen after you hit retirement (it just looks at each year and compares to your withdrawal rate to test if you can retire - which of course won't reflect the average as you've just highlighted), but this would be a great idea for enhancing it!

I still think that $1 mil is a great target to aim for, and will be trying to follow in your slip-stream! Hopefully I’ll fall across the line only a few years after you!

Cheers,

Jason

I saw your post today, and have to dig in to it. I really liked your last calculator so will give this one a spin, too.

DeleteI'm not actually sure we're ahead of you in the investment realm, though it doesn't really matter either way. With some luck, we'll both hit the $1M mark in 2021. :)

I always think of fitness as a way for me to be frugal about my hobbies, but in the span of a year the membership fees and supplements really rack up your costs! I'm not too sure if that's where you're fitness budget went, but I know that's where mine went.

ReplyDeleteps. Yay for budget porn!

Hi Anum. We end up getting creative with where we put each expense. So that fitness figure is gym memberships, new running shoes, even stuff like hiking gear. I think our new two-person backpacking tent made its way in there, which kind of skews the figures...it was over $300, if I recall.

DeleteAnd yes, hooray for budget porn. That's the only peek you get all year.

DeleteOur aim is closer to a 3% WR and I feel like we're adding a layer of safety in that we're including in our expenses our mortgage payments, which amount to ~$10K/year. So we'll save up 25x$10K for that portion of our current spend specifically, but will only need to pay off the mortgage for 7 years after we FIRE. Thereafter that money will be a pretty significant buffer against other large and irregular expenses.

ReplyDeletePS - What is $610 in "annual charge"? Totally curious!

Delete3% really ought to be the 4% for early retirees. Though then we'll have to save so much that my blog will need a new name.

DeleteWe are hoping our rentals provide another layer of safety, but the more we get the less I like them and the more I appreciate the simplicity of an index fund. I could just as easily see us jettisoning them by the time retirement rolls around.

Oh, those annual charges are for our travel hacking: so two $75 fees for the Club Carlson cards, two $89 fees for the US Air cards, $95, I think, for the British Airways card, etc. They really add up.

Really good post and it gives me a nice point to think about my own spending and what I will need. Of course I am a bit further away and need to be debt free first. Probably another decade for this chap, but it could be worse.

ReplyDeleteA decade is still a very short runway to financial independence. Ours was longer, and also involved debt.

DeleteBest of luck, Jason!

You've made some great points here. We are also hoping to retire early (age 46) but out biggest unknowns are things related to the kids. Hard to plan for college when they are only 3 and 5. We have a ways left to go - around 12 years - so all we're doing now is saving and investing as much as we can.

ReplyDeleteThanks, Holly. Kids are a huge unknown for us as well. If you figure out how to estimate and plan future college costs, please write about it and let us know!

DeleteI've calculated what I need to save to have a 4% SWR and am targeting that plus a paid off mortgage. Once I get there, I'll do a more realistic budget. My budget actually involves a lot of forecasting for infrequent things like passport renewals and cable modems, so it's not a bad picture. The main thing it ignores is car replacement, which is something I'll evaluate later. Since I live in a big city, it's not a big deal if I don't have the $$ to buy a car upfront.

ReplyDeleteThat's great that you have future costs in the analysis already, leigh. We don't, I think in part because I don't necessarily want to hold the cash and suffer opportunity costs for a 'future roof' savings account. They're probably a way to account for the costs without actually saving for them.

DeleteI figure you're in a better position, given the way you budget currently.

Interesting thoughts!

ReplyDeletePersonally I think you are being way too pessimistic. Are you really going to be spending $7000 a year on travel, bearing in mind you will be at leisure to travel at any point in time, so going off peak and getting the best deals? Or if you are planning on travelling the World you will be taking advantage of cheaper prices in certain countries, and combined with your grocery, date night, restaurant, and loads of other costs will be non existent in those months you are away, you will probably come out with a lower budget than your current one anyway (you can also rent out your house while you are away to bring in even more money).

Another point is that are you really sure you will never earn another penny once you quit your day job? You and Mrs DB40 sound like productive people and I am sure you will both want to do something on the side to keep you busy, which will no doubt bring in a little extra money. A small side business that could take say 5-10 hours per week could easily bring in $5000/year which would cover any unforseen expenses, and is worth $125,000 worth of extra savings. That could see you working an extra 3-5 years if you want to save that up, personally I'd errr on the side of getting the hell out of there asap but maybe you don't mind your job as much as I dislike mine ;)

True, I could definitely be overly pessimistic. Or I could be optimistic...

DeleteThe rub is that, with only $31k of spending, the range for pessimism is much smaller than the range for optimism, if that makes sense. That is to say, my 'true' spending might very well turn out to be slightly less...say, $25k. But it's not going to be way less than that.

However, I could be way off on the other side, too. True spending could be $40k or 50k when we account for healthcare costs, children, college educations, etc. There's a way bigger range above my estimated spending than below....and way worse consequences. So, pessimism is safer.

We will have other income streams though, as you note. Rental properties, maybe some actual work income, social security (eventually). So, there are buffers in place, and some reasons for optimism.

I really appreciate the call for being positive, FIREstarter.

Just realized this too, I haven't been tracking my yearly spending though I have a monthly data of it. I guess it's really important to compute this number and then still work around it to arrive with your final spendings projection.

ReplyDeleteI'm glad I'm not the only one. Great minds!

DeleteIt wasn't so bad, once I figured out how to organize it. I just laid out each month's spending in a new column, and had a formula to add up everything in the rows.

The tricky part was when I added in a new row in certain months for one-off expenditures. For 2015 and beyond, I'm keeping every category the same month-to-month.

Sounds like your numbers are sound: I like the $37,500 number - that should give you enough to sock away for the extras when they come. Did you factor in extra groceries/living expenses for if/when you decide to have kids?

ReplyDeleteNot yet, Laurie. I really am throwing darts with any children expenditures. I could see things being pricey, or not that much of an increase at all.

DeleteInteresting...it's something I've been meaning to do too. We don't really track our expenses as well as we should. Our expenses are higher mainly due to mortgage and stupid co-op maintenance fees. I was trying to figure out a number too as I'd like to retire early or just reach early FI, whatever you want to call it. I agree that the just using your expenses and figuring out the withdrawal rate is a bit simplistic. Plus, it's sometimes hard to project what expenses may come with kids as they grow up. As for me, if I retire early I'll take a big penalty with my pension but can still add in pension income at age 55. Also, I will hopefully have some rental property and add that in. Are you taking rental income into account and are you planning on buying more properties?

ReplyDeleteHey Andrew! Congrats again on the new home!

DeleteKids are a big unknown for us, especially since they don't yet exist. Those jerks are messing with our money pre-existence.

Any rental income (or other income) is outside this analysis. I'm tempted to reduce the amount we actually need from our investments by that amount, but thought it might serve as a better buffer.

We're currently planning on getting more rentals but, to be honest, the longer I hold them, the better I like index funds. :)

I'm glad there is some money in there for health, enjoyment, etc. You spent a lot on travel but think of the great memories you will have!

ReplyDeleteYeah, travel is a big priority for us and probably the best money we spend. But it's a little high. As we do more travel hacking, we should get it more in the $5k level annually.

DeleteWe are our own worst critics. Just because you will leave "employment" early, doesn't mean you aren't going to continue to find unique and creative opportunities to produce side income for the unexpected financial challenges (and opportunities!).

ReplyDeleteYou can never plan for everything, but you can plan on dealing with what comes confidently given your skills, emergency stash, and craftiness.

S.O. and I both left employment without planning to 3 years ago and despite lower annual income than when we worked full-time, we have managed to save more, invest more, and cover the "emergencies" without any real stress. Our priorities are more aligned, which drives better spending choices to preserve them :)

Emily! Really glad to hear from you.

DeleteIt's great to hear from someone that's left the rat race that income still happens. It's one of my big, irrational fears: that money will stop flowing into our household once I leave the corporation.

I definitely do not want to commercialize my writing, as I enjoy it so much. The last thing I want to do is taint it.

But there are other things we could do that could bring in cash. And maybe it'll turn out like it did with you and your SO: maybe we'll save and invest more when we align our actions with our real priorities.

How does inflation factor in? I feel like maybe that's in the 4%, but don't really know?

ReplyDeleteHi Femme Frugality. :)

DeleteI think the 4% Rule assumes that a balanced portfolio will earn 7% in an average year, allowing for 3% inflation. I'm certainly no expert, but that's my read on it.

Gotcha. I'm such a newb to the retirement game. Definitely staffing away for it but have yet to really define a plan to get our of the game.

DeleteSacrelige?

Not at all. I think that's the theme of the post: trying to understand where your knowledge gaps are. We all have them.

DeleteWe've been calculating higher costs in early retirement since we'll be on a homestead and there'll be start-up expenses associated with that life (building materials, equipment, etc). But, we also don't plan to be entirely sans income--it'll just be drastically reduced, not full-time income. I like your conservative estimates and it seems like you're on the right track.

ReplyDeleteWe spent $13,000 in 2014, but that doesn't include our mortgage. Since we'll likely be mortgage-free in early retirement, we're more focused on our actual living expenses at this point.

Hi Mrs. Frugalwoods,

Delete$13,000 is incredible. Well done.

I fully expect our expenses to go up in retirement (unsubsidized health insurance for us + kids, college savings, and the sort of things I mentioned above). But I could be overly conservative.

I figure if we saved too much, no big deal. :)

I sorta feel like I coulda/shoulda look at my annual expenses... But I tend to look the other way, you know, I netted this much post tax, and then I paid $x on the mortgage, so the rest was what I spent... Saves the need to be meticulous on the day to day outgoings... Sadly, I seem to do them in different annualised windows - my mortgage spreadsheet runs year on year from Christmas (anniversary of remortgaging), and then my pay goes into a spreadsheet for our FY which is July through June. But I should crunch them together somehow!

ReplyDeleteOk that was scary! Since Xmas, I've earnt (after tax)

$28k, and my mortgage costs have been just over

$6.5k, and I've paid

$6.5k for rent + food into our shared account

I should have $15k in savings - ha! My mortgage offset account has grown about $3k. Holy moly, this is a wake up call. There is about $2 in travel costs in there somewhere, but still!

Hi Sarah! Good to hear from you.

DeleteFirst, great income there since Christmas.

I am a BIG proponent of actually creating and following a budget, as I've found that there are almost always 'leaks' in our bank accounts. Without tracking, there is little opportunity for improvement. The laissez faire approach is often good in theory, but costly in practice.

I really like this post DB40, one of my favorites if not thee favorite. I like the IRS depreciation method of figuring out expenses I could see that being a really good idea to calculate for everyone.

ReplyDeleteIn my own calculations, I go with the assumption that I'm wrong and instead budget the 1 year's worth of expenses as an emergency fund, then top it off with assuming i'm half right on my annual expenses, ie your 31K would require me to have 62K per year, I know it seems like too much, but I have been wrong in the past why not have extra cushion for it.

That approach will definitely create a good cushion! Still, to create $62k annually would require about $1.55M using the 4% rule. It's certainly possible, but it would mean we'd be 'done' sometime mid forties or so. :)

DeleteMy wife, crazy woman that she is, may actually want to work several years after I leave the workforce. So, who knows, maybe we can make your plan happen.

The ways to count for retiremen are indeed as different as the ways we live and intend to live our lives. I do not work much any more but I do count assets (I have no debt) simply as how many years will it sustain me using a probable budget, not the actual costs. Your point is important, but don't forget to count inflation over say 30 years on the annual budget too.

ReplyDeleteInflation is a huge factor to consider, and luckily one that is somewhat addressed in the 4% rule (which assumes 3% annual inflation, I believe). Nonetheless, this is no substitute for real financial planning, especially as we're living in a time of abnormally low inflation.

Delete