It's a great feeling, if a little more subdued than we thought it might be. Maybe it's because we'd been mortgage free once before. Or maybe it'll just take some time to sink in.

Maybe we're a bit distracted as Mrs. Done by Forty was offered a job on the same day, and her decisions on that are more pressing than celebrating a milestone.

Maybe we're a bit distracted as Mrs. Done by Forty was offered a job on the same day, and her decisions on that are more pressing than celebrating a milestone.

We did celebrate, of course. We made a fancy dinner, opened a bottle of champagne, and like any loving couple does, competed ruthlessly against each other in a board game about corporate domination of space:

|

| Mrs. Done by Forty won. It wasn't close. |

After sending in the final payment, I figured I'd go to the Mad Fientist's laboratory and see how these changes would impact our timeline to financial independence. Since our mortgage rate was 3.75% and it was a very new mortgage, I assumed it wouldn't really impact our projections very much when working towards the 4% rule. The spread is only a quarter percent, right?

Right before paying off the mortgage, here's what the Mad Fientist's laboratory predicted for our FIRE plans a couple weeks ago on June 30th:

|

| Click for bigness. |

One year and one month isn't too shabby. This would be under the assumption of the 4% rule and we are planning for 3.5%, but still.

So let's see what happens to your financial independence plans when we take about $262,000 out of your portfolio all at once. Here's what the Mad Fientist's laboratory projected under that scenario:

|

| Click for bigness. |

Yikes. Using a big chunk of our portfolio to pay off our mortgage would push our FI plans out by a year and a half.

Right after putting those figures in, I started feeling some regret.

But wait! Paying off our mortgage doesn't just reduce our portfolio...it also reduces our expenses. What happens if I take that red expense line from the Mad Fientist graph (which is a rolling average of our last twelve months of spending), and reduced that by the amount of principle and interest we paid each month ($1,267).

What would would happen to our timeline then?

What would would happen to our timeline then?

|

| Click for bigness. |

Um.

Wait, what?

Does this mean we're financially independent? How did this happen?

I think the reason paying off the mortgage accelerated our progress towards financial independence, at least on paper, is that the $262,000 we still owed resulted in an annual principle and interest cost of $15,200, too.

Four percent of $262,000 is only $10,480: a good bit less than the $15,200 we would be paying in P&I over the next 28 years or so with the mortgage. So eliminating that annual cost, while certainly shrinking our portfolio quite a bit, seems to still have gotten us ahead.

Another way of putting this is that to cover our annual P&I expense of $15,200, using the 4% rule, we'd need $380,000 invested: roughly $118,000 more than it would take to simply pay off the debt. This would, not coincidentally, take us a bit over a year to achieve at our current savings rate (and presuming the market also returned 7% during that year on our portfolio): basically the amount of time the Mad Fientist's laboratory was telling us it would take to hit financial independence.

In other words: the reason we'd have to work an additional 13 months to hit financial independence was because we were planning on saving up enough to cover the annual mortgage expense with additional investments, instead of just paying it off.

In other words: the reason we'd have to work an additional 13 months to hit financial independence was because we were planning on saving up enough to cover the annual mortgage expense with additional investments, instead of just paying it off.

I was, and am, somewhat surprised to see how eliminating the mortgage seems to have, maybe, sort of, made us financially independent under the 4% rule. A few caveats though:

- The current calculations apparently are predicting our new, mortgage-less budget will only be $32,256 (or what would have been $47,456 with the P&I). Even though this figure is truly what we spent the past twelve months minus principle and interest (and that year includes some weird expenses, like hitting our out of pocket maximum for Baby AF), we want to assume a little higher figure just to have at least some cushion.

- There are going to be new expenses once we leave work that aren't showing up in the past twelve months of our budget: like buying our own health insurance, replacing the car at some point in the future, eventually having to buy a new roof, a new AC unit, etc. Just like every other, this year isn't average. Almost all early retirees are probably underestimating their future expenses if they're using their prior years as a baseline.

- Most critically, while the Mad Fientist's lab defaults to the 4%, we are planning on using 3.5% in our assumptions.

Still, these are all things I can dive in to in future posts. There will be a lot of time for pouring over the details of our new plan. The bottom line is that we still have some work to do to be truly financially independent.

Still, while I definitely don't want to dole out advice on whether other people should do with their mortgages, I'm surprised by the results. Everyone is going to have their own unique interest rates, will have purchased homes at different prices, and everyone's going to be at their own place in their amortization schedules. Some people will have just gotten their mortgages, some will be close to paying it off.

I'd say that if you're working towards financial independence and have a mortgage, don't be a dunce like me and wait until you send in the final payment to figure out what the impact will be. Look at your current mortgage balance, and take some time to do the math.

We all have our own feelings on debt. Many of us like leverage, especially if we can get it at low interest, and want to use that lever to maximize gains all the way through financial independence. Others of us are fairly anti-debt, and will try to get all of it out of our lives if we can, opportunity costs be damned.

Either way, do better than I did. Take out a calculator, and let the math do the talking.

Congrats on paying off the mortgage! That's so awesome. Being debt free must be pretty exhilarating. I know because ever since we bought our house last August, my worry over the mortgage has increased significantly. It's definitely a chain.

ReplyDeleteHi there, SFL. I have to admit that it's more a surreal feeling that all that exhilarating right now, but it's still so new: I imagine things will sink in over time.

DeleteCongratulations on the new home! I know what you mean about the worry with the mortgage, for sure. For what it's worth, I think that subsides, too.

Hi There, great job on paying off the mortgage and moving closer to FI (or perhaps reaching it depending on the math). I have a few questions based on what you've said here.

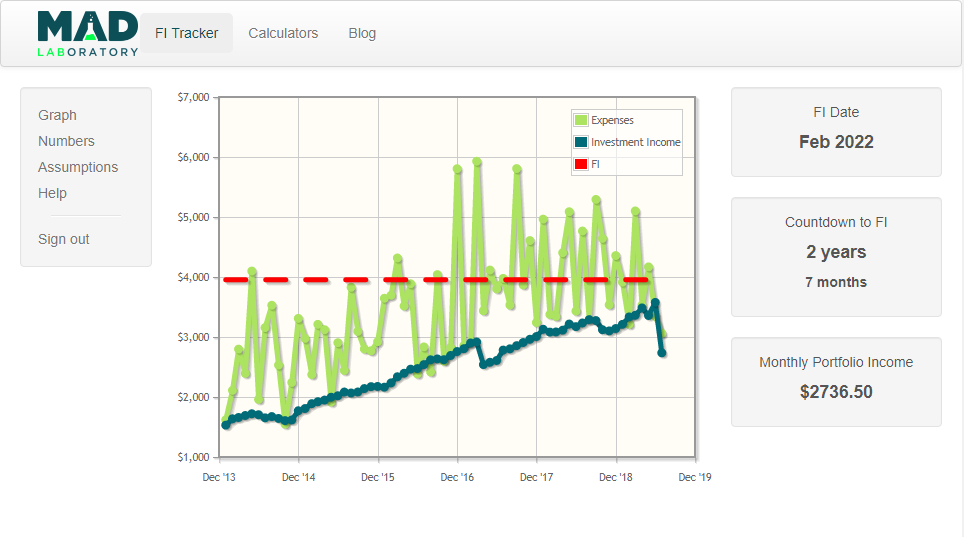

ReplyDeleteThe red line in the graph is one of the variables that we can set, not a running average that is auto-calculated, so do you recalculate a running expense average regularly and then update the expense number yourself?

Also, you said that the withdrawal ratio is set at 4, but that is editable as well. I have mine set to 3 for instance.

Finally, and most importantly, what is the name of that game you were playing with your wife? I'm always looking for table games to play with the family.

Thanks and good luck with your journey.

Hi Nelson! Thanks for the comment.

DeleteThe red line in the graph auto-defaults to a running average of your prior 12 months of spending. Only if you enter in your future expenses as one of the three "assumptions" does it change to your entry.

And yep, I realize that you can also change your withdrawal rates. (See prior "Are we on track for FI" posts to see the graphs for 3.5%. I thought of including one here but I'd already thrown 3 graphs at people and thought it might be a bit much to add another.)

That game is Terraforming Mars: one of our recent finds and already in our very top tier for board games. It's amazing. We play at least a little almost every day. :)

Congratulations! Great job paying off the mortgage. I'm sure you won't regret it. We'll have a similar choice very soon. Our old condo is under contract. We'll have the option to pay off our mortgage or invest. I'm leaning toward investing, but I need to do a bit more research.

ReplyDeleteI don't really trust any retirement calculator. They all seem very optimistic. :)

Thanks, Joe! Yeah, it sounds like we have some similar recent experiences with real estate: a lot of the funds we have available are here because we sold our two rental properties. We decided we just didn't like being landlords. Not a great fit for us.

DeleteAnd I kind of agree on retirement calculators. We tend to be more conservative (shooting for 3.5%, and will add some money to our actual budgets just to be conservative and account for the things we know will eventually come up like new cars, appliances, home repair, health insurance & healthcare costs, etc.)

Huh. I’d never thought about it that way, but it inherently makes sense. Our mortgage sits at 3.375%, even below that 3.5% mark. Hmm...

ReplyDeleteHi Angela!

DeleteEven more than the interest rate, I'd say how close you are to financial independence + how 'far' you are into your amortization schedule probably tips the needle on whether to pay off early or not.

Like, if we only had $60k left on our original $272k mortgage, I think it would be a no brainer to pay it off around our FIRE date because we'd still have 5+ years of paying the same $15k of P&I.

Anyway, the math was surprising to me so I'd be interested to see how other people's math shook out.

We're in a similar late stage payoff debate. We've decided to just payoff the remaining $25k of an originally 110k mortgage using our "probably bigger than it needs to be" e-fund and a small windfall of backpay expected this summer. We're still 6 years out from our planned FIRE date but it's based on a years-of-service threshold that we want to reach instead of purely asset based.

DeleteI like that decision, Thomas. An emergency fund is a good thing but your cashflow immediately improves without a mortgage: easy to rebuild and, if the market corrects, you'll be able to buy more on sale.

DeleteCongratulations! I enjoy your posts and find them very thoughtful. Have you written about how you estimate the future cost of healthcare in retirement?

ReplyDeleteThanks for the kind words, friend.

DeleteI haven't written about that yet, because so much is in flux (like, the sudden appearance of Baby AF and the possibility of his future accomplice, MC Baby). But the short answer is that we plan on buying healthcare through the ACA marketplace and will presumably get some sort of subsidy in the process.

I started playing around with the ACA website last December but didn't get far enough as to actually get quotes. Maybe I'll give that another go this December.

Congratulations!

ReplyDeleteI'm firmly in the "retire with a paid-off mortgage" camp. It makes a HUGE difference to your security and expenses.

Thanks for stopping by and commenting, Frogdancer!

DeleteI've gone back and forth on the issue over the years but now that we're so close to FI (and that we've seen it actually accelerates our timeline to FI a bit) we're pretty firmly in that camp, too.

I certainly wouldn't advise a 65 year old, just about to retire person, to take a mortgage out on their paid-off home and leverage up going into retirement. So why should I keep it around if I'm about to retire?

This comment has been removed by a blog administrator.

ReplyDeleteCongratulations on paying off the mortgage. Is the job offer something to do with your wife's Ph.D.? Professor? What board game was that BTW?

ReplyDeleteHi, Jason!

DeleteMrs. Done by Forty still waiting to hear about salary and she's not really sure if she'll take it, so I'll stay pretty mum on the details. It's not a professor position though.

Oh, and that game is Terraforming Mars. Highly recommend if you're into boardgames.

Congrats on paying off the mortgage and on achieving FIRE (on paper at least)! Look forward to hearing about your future plans.

ReplyDeleteThanks, Andrew! Good to hear from you, friend. How are things with the fam in NYC?

DeleteI hesitated to even call us FIRE in the post because we don't really yet: maybe "4% FIRE" or whatever but we've got a little ways to go. Still, I did want to write a bit about how paying down the mortgage seemed to have sped things up because I'm sure other FIRE folks are facing similar situations.

Woot! So exciting!

ReplyDeleteIt must feel great to be mortgage free. I'm about 6 years out from that if I want to prioritize retirement (and I do). But I'm psyched for the big day, even if it's a bit far out.

Glad you're planning for more expenses in the future. I always worry about that with early retirees.

Thanks, Abby!

DeleteI think it's smart to make sure retirement is also prioritized. You can retire with a mortgage but you can't retire without a way to cover your expenses.

And six years isn't all that far!

I agree that a lot of early retirees are missing out on costs that are coming (ironically, because their path to FI is so short that it often doesn't ever show up in their budgets on the way to FI).

we paid off our mortgage about 4-5 years ago, but ours was from the early 2000's and i think over 6%. we had very little left (under 50k) so refinancing made no sense with closing costs and all that. now just make sure you have cash on hand for those major repairs. they will come and sometimes come in waves. ask me how i know!

ReplyDeleteCongrats on your home payoff as well, freddy.

DeleteWe have very little cash at the moment (just a pile of investments) but will be building the cash funds up over time now that we have better cashflow. :)

Belatedly, congrats!! Has the coolness of being mortgage free sunk in yet?

ReplyDelete4% of our mortgage is $11K less than our annual P&I but we would more than halve our invested assets to pay off the mortgage at this stage in the game so I've got to stick it out and see where we are in about five years or so.

Thanks, Revanche! I don't know if it's sunk in quite yet, but I think next week when I don't send in my mortgage payment, it might start to feel like it's real.

DeleteI see what you're saying about having to put much more of your nest egg towards mortgage payoff. $11k is certainly nothing to snub your nose at but putting half of what you've got into one asset is a big move and the taxes could be pretty hairy, too.

A good reminder that a big reason we could make this move is that we're in the relatively LCOL Phoenix metro.

Thanks for commenting, friend!

Congratulations! I'm glad there was a positive outcome in the end. Your post was a roller coaster of emotion and I was really worried for you when your time to FI increased! Zero sounds much better.

ReplyDeleteThanks, Daizy! We're probably still a year and a half away from what we personally would define as financially independent (basically with the 3.5% SWR). But I figure when I started the blog I was working with the 4% in mind when I came up with the done by forty goal: might as well celebrate that milestone if it's technically the goal we started with.

Delete